Sustainability data to drive decisions, not just disclosures

Capture private customer data and access public sustainability disclosures to power sustainability reporting, transition finance, and supply chain decarbonisation.

.avif)

.avif)

.avif)

.avif)

.avif)

The Challenge

When sustainability data is incomplete or unreliable, decisions in reporting, financing, and risk management break down.

Public datasets are often out-of-date and inconsistent. Private data is expensive and difficult to collect. Every gap adds more work, greater uncertainty, and less confidence in the numbers. It’s no surprise that a third of financial executives don’t trust their own sustainability data.

ESG Book unifies the public and private sustainability data you need, in one platform, delivering higher accuracy, less effort, and full source documentation. Spend less time chasing data and more time using it.

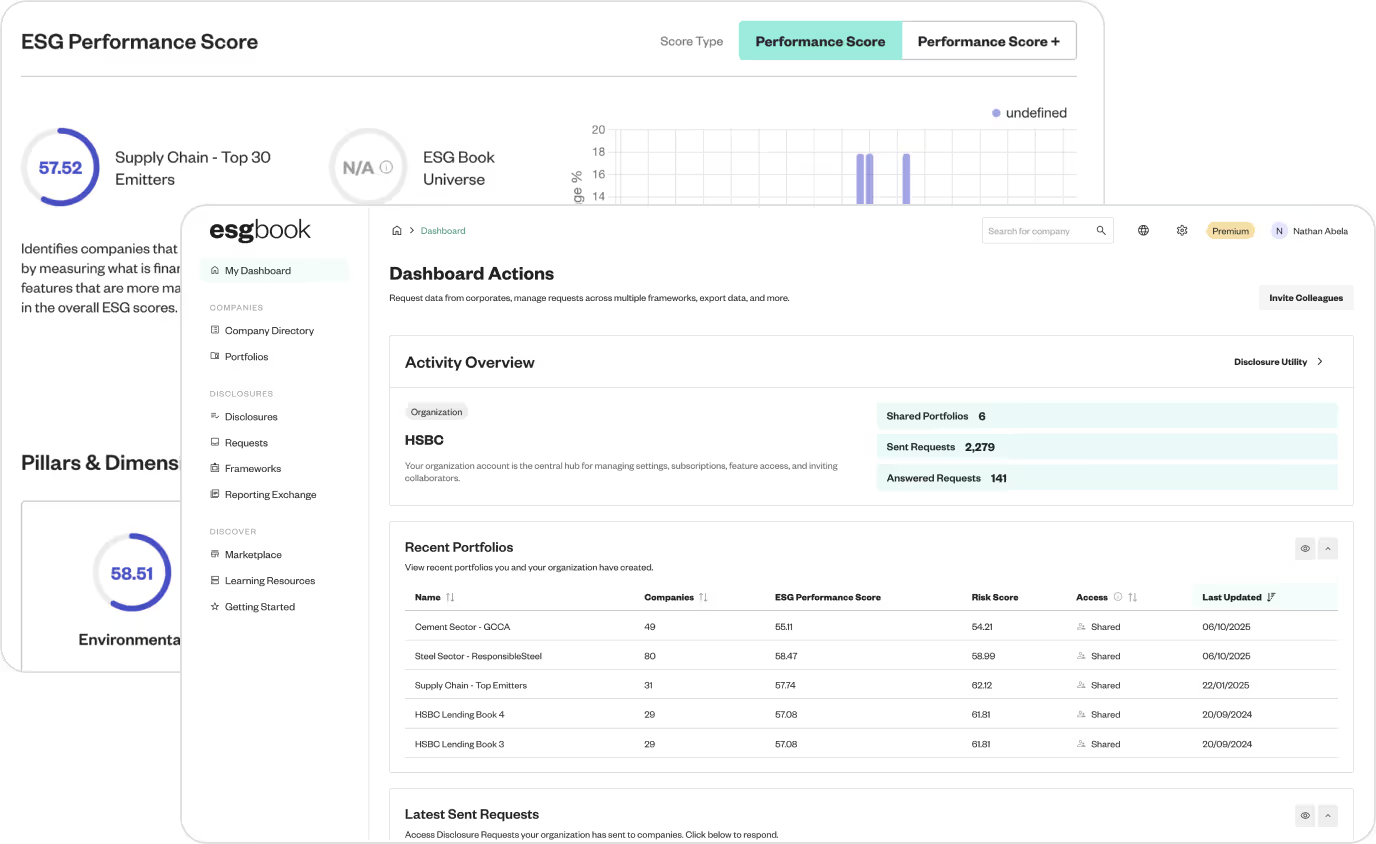

Sustainability Reporting

Access and collect validated customer sustainability data - public & private - mapped to your reporting frameworks.

Increase coverage and completeness, automate reporting, and cut the manual work involved in regulatory submissions.

.avif)

Transition

Finance

Finance customers’ shift to lower-carbon operations and measure their performance against emissions targets.

Use validated emissions data in underwriting to grow sustainability linked lending volume, track borrower progress, and flag missed targets.

.avif)

Supply Chain Decarbonisation

Engage suppliers and report on your own Scope 1, 2, and 3 emissions.

Automate public and private data collection, use real data for reporting instead of spend estimates, and flag high-emission suppliers.

Close Data Gaps

Build Trust in Data

.avif)

Pricing that Scales

Ready to simplify reporting and regain trust in your sustainability data?

“As the demand for reliable and comparable climate-related information continues to grow, a standardised data request and reporting template is essential...This is especially valuable when requesting data from privately held companies, where these disclosures are often limited."