Breaking New Ground

In 2024, the global sustainability landscape underwent significant transformation, with governments, regulatory bodies, and organisations worldwide taking major strides in sustainability reporting, standard-setting, and policy development. Last year marked the continued evolution of the International Sustainability Standards Board (ISSB) framework and the adoption of the Corporate Sustainability Reporting Directive (CSRD), both of which redefined the trajectory for environmental, social, and governance (ESG) reporting.

As jurisdictions began to embed these global standards into their legal and regulatory frameworks, ESG Book maintained a close watch on these developments. Our ISSB Adoption Tracker has become an invaluable resource for monitoring the global uptake of IFRS S1 and S2, highlighting trends in adoption, alignment, and jurisdiction-specific adaptations. Meanwhile, ESG Book’s CSRD Transposition Tracker chronicles the varying progress of EU Member States in implementing the directive, shedding light on opportunities and challenges in harmonising sustainability disclosure across Europe.

In this retrospective, we explore the milestones, challenges, and future outlook of sustainability reporting. From the ISSB’s push for global alignment and the European Commission’s efforts to streamline sustainability frameworks to the increasing regulatory focus on ESG ratings and biodiversity disclosures, this report provides a comprehensive review of the regulatory shifts and innovations that defined 2024.

The global ESG landscape stands at a critical juncture. The shift from voluntary to mandatory reporting, the emergence of interoperability between standards, and the ongoing efforts to balance compliance with innovation are reshaping how companies, investors, and regulators engage with sustainability. Join us as we reflect on this transformative year and look ahead to the key deadlines, challenges, and opportunities that lie ahead in 2025 and beyond.

Global ISSB Adoption

Since the ISSB standards were first issued in 2023, many jurisdictions are adopting or integrating these standards into their legal or regulatory frameworks. A key focus for regulators is achieving comparability across entities and jurisdictions, which is crucial for attracting foreign capital and managing cross-border activities. Adopting ISSB Standards helps reduce regulatory fragmentation and provides a passporting mechanism to align various reporting regimes, aiding companies and investors.

ESG Book’s ISSB Adoption Tracker is a living document that monitors the regulatory implementation, adoption and use of the International Sustainability Standards Board (ISSB) standards - IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information and IFRS S2 for Climate-related Disclosures - across global jurisdictions. Currently, 28 jurisdictions worldwide have decided to use the ISSB standards or are taking steps to introduce them in their frameworks. These jurisdictions account for roughly 55% of global GDP, over 40% of global market capitalisation, and more than half of global greenhouse gas emissions1. In this data visual, we look at the state of adoption of the standards around the world in 2024.

The ISSB framework does not explicitly present a binary choice between adoption and convergence. Instead, the ISSB acknowledges a spectrum of jurisdictional approaches towards implementation, which may include:

- Adoption: Full incorporation of ISSB standards into a jurisdiction’s legal or regulatory framework, requiring entities to apply these standards directly.

- Other use: This includes varying degrees of alignment or integration of ISSB standards into local frameworks. For instance, jurisdictions may:

- Align national standards closely with ISSB standards without fully adopting them.

- Permit the use of ISSB standards alongside existing local requirements (a form of dual reporting).

- Introduce modifications to ISSB standards to address specific jurisdictional needs.

The Jurisdictional Guide published by the IFRS Foundation highlights this flexibility. It categorises approaches based on features like the degree of alignment, regulatory or legal standing, and any jurisdictional modifications or additional disclosure requirements introduced. While the ISSB emphasises adoption as the ideal outcome for achieving global comparability, it accommodates jurisdictions that choose alternative pathways to align their local frameworks with ISSB standards. We track the variability of alignment through our ISSB Adoption Tracker, which includes insights into the gold-plating of standards across different jurisdictions.

To learn more about ESG Book’s ISSB Adoption and CSRD Transposition Trackers, contact info@esgbook.com.

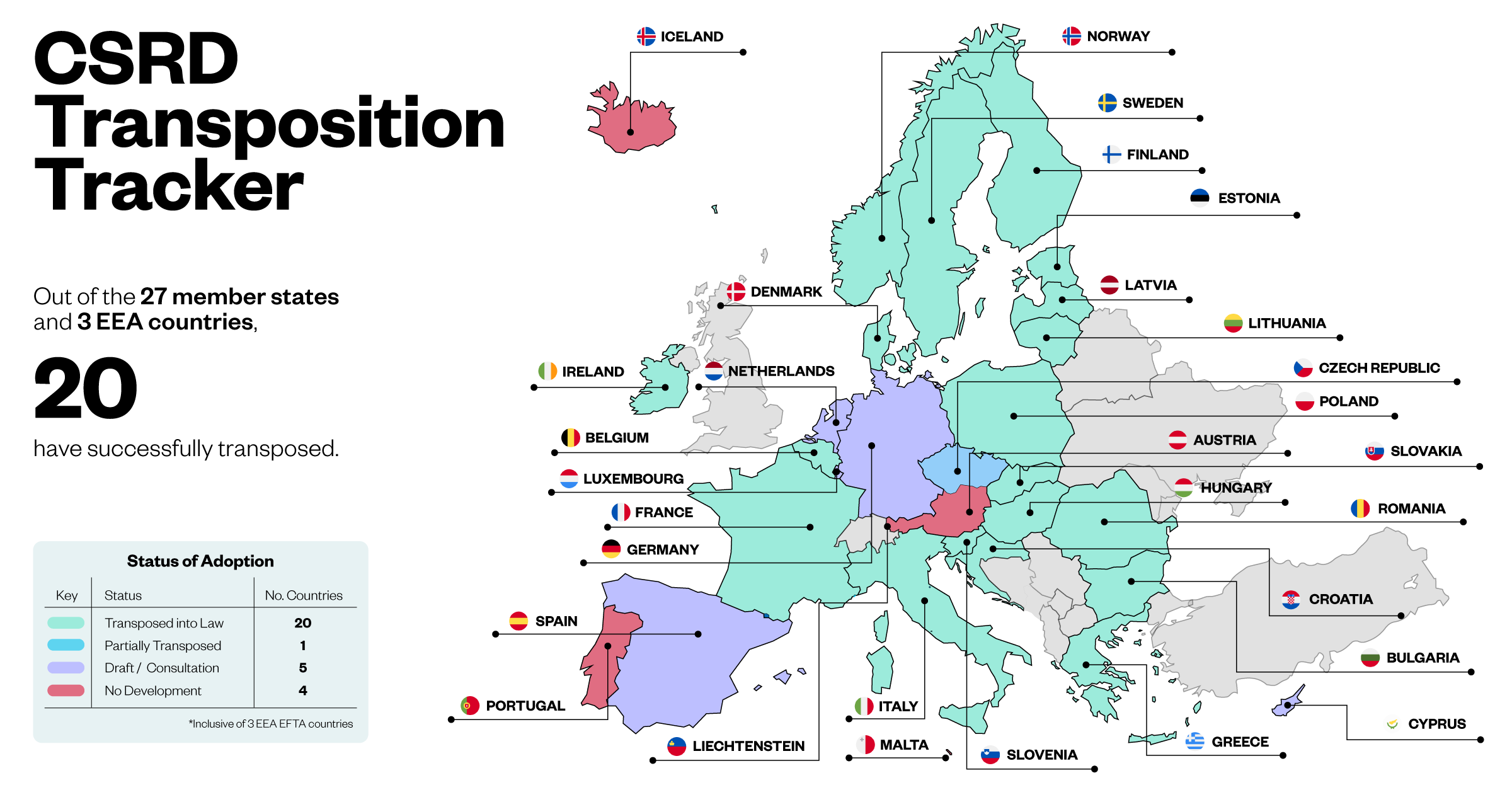

CSRD Transposition

So far, 13 Member States have fully transposed the Directive into national law: Norway, Sweden, Finland, Ireland, Denmark, Lithuania, France, Slovakia, Romania, Bulgaria, Italy, Croatia, Cyprus.

In December, Greece and Spain introduced legislation to transpose the CSRD into national law, following criticism from the European Commission for several Member States missing the July 6th transposition deadline. Meanwhile, as of December 2024, Belgium, Poland and Slovenia have successfully adopted the CSRD.

In light of CSRD’s relatively lacklustre adoption, there are a few EU Member States whose CSRD transposition needs a kickstart: namely, Portugal, Austria and Iceland. The Politics of CSRD: A leaked letter from German legislators revealed a last-minute effort to narrow the scope of the Directive, proposing that it apply only to companies with 1,000 or more employees and that implementation be postponed by two years.2

While German ministries are urging the European Commission to ease the reporting requirements, it is unlikely that this will affect the transposition, given that the letter comes from an outgoing government.

European Commission’s Omnibus Regulation: Streamlining Sustainability Reporting, or a step backwards?

Given consistent corporate and political pushback throughout 2024, the European Union has announced plans to streamline reporting through an omnibus package to address the overlapping needs of SFDR, the EU Taxonomy, and the CSRD. Proposals for this omnibus package are officially scheduled in February 2025, with further developments likely taking place throughout the year. Will this help reduce the reporting burden or become a bureaucratic misstep? Overall, we expect certain minor amendments to the European Sustainability Reporting Standards (ESRS) at most, aligning the reporting framework with the existing components of the EU’s sustainable finance package. It is unlikely that regulators will introduce significant changes with the first reporting deadline fast approaching.

The first wave of large companies subject to the CSRD in 2025 must proactively gather data to report on material topics under the ESRS. The European Commission’s consolidation effort ultimately aims to reduce administrative burden and bureaucratic complexity, thereby easing compliance for smaller companies subject to the CSRD.

.png)

State of the Union: A New Era Under Trump

The United States is poised to enter a period of patchwork policymaking, with states leading climate initiatives as federal regulations face potential setbacks or outright reversals under Trump appointees at agencies like the Environmental Protection Agency (EPA) and the Securities and Exchanges Commission (SEC).

As President Trump begins his term in 2025, the trajectory of ESG regulation in the US may slow significantly or even face potential reversals. This recent

article on the US elections highlights our projections regarding the potential rollback of environmental regulations and initiatives. These include the Clean Air Reduction Act, which introduced methane emissions fees and an Executive Order renewing increased exploration and extraction of fossil fuels on federal lands, and a broader pivot away from climate diplomacy and multilateralism, in favour of President Trump’s “America First” approach and policies. Meanwhile, the fate of the SEC’s climate disclosure rule still hangs in the balance. The regulation has successfully cleared its first legal challenge. However, as the new year unfolds, the 2025 implementation deadline seems increasingly unrealistic. With Gensler’s imminent departure, a new Trump-appointed SEC chair could potentially dismantle the rule or shift to a lighter-touch, principles-based regulatory approach. That is, if the rule survives at all.

California Corporate Climate Accountability Package (CA SB 253, CA SB 261, CA SB 219): California legislators have set a national precedent by introducing mandatory climate reporting requirements. These regulations mandate emissions reporting from 2026*, including value chain emissions, for companies with over $1 billion in revenue, and TCFD-aligned disclosures for companies exceeding $500 million in revenue. Home to some of the largest Fortune 500 companies affected by these rules, California underscores its commitment to climate leadership. The state has made it unequivocally clear that addressing climate change is a top priority, even as federal regulators grapple with political and legal obstacles. Similar measures are now being mirrored in states like Illinois and New York, signalling a growing momentum for state-level climate action.

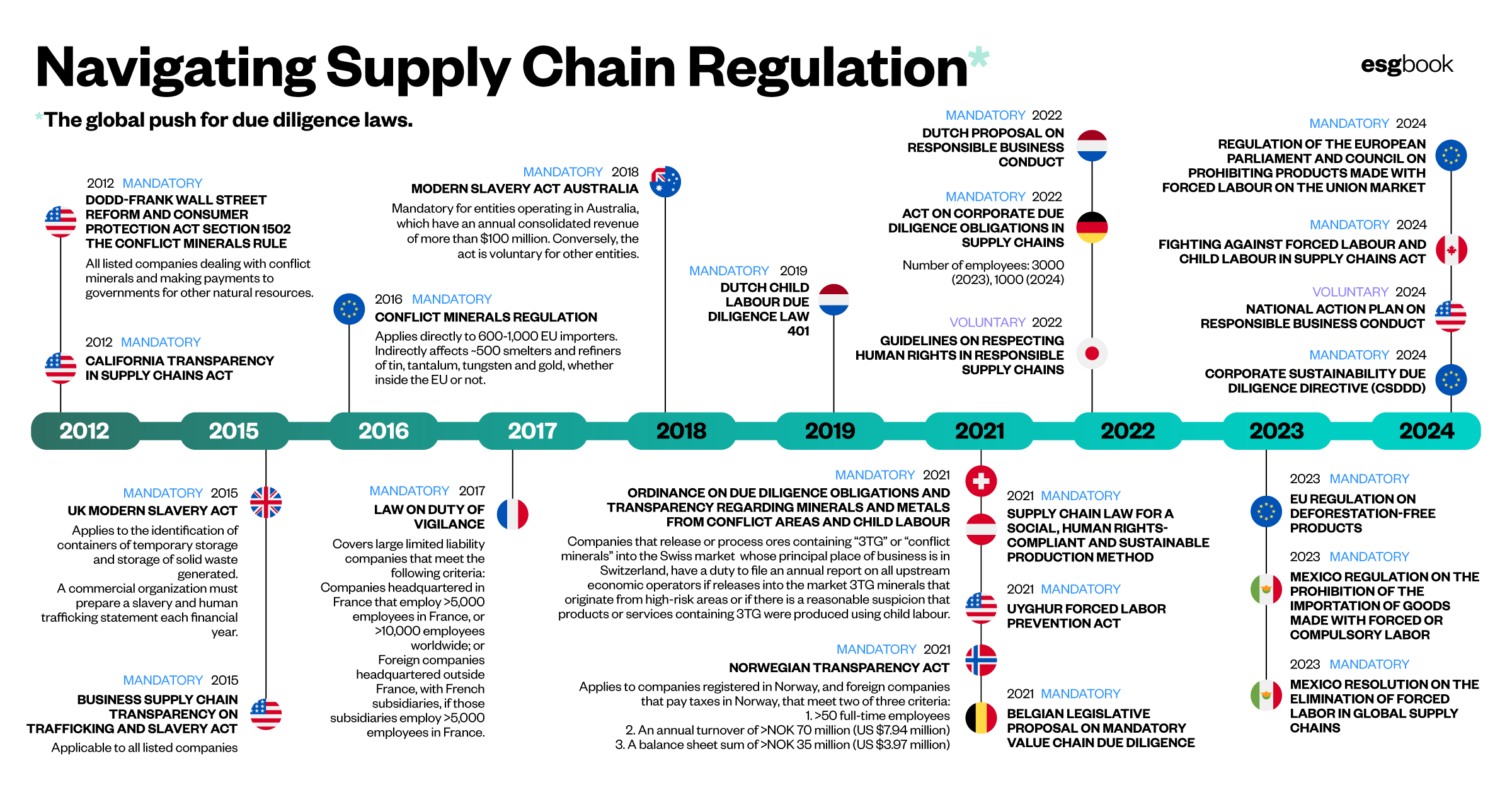

Global Supply Chain Regulation: Due Diligence and Beyond

Mexico Regulation on the Prohibition of the Importation of Goods Made with Forced or Compulsory Labor” (May 18, 2023) – This regulation bans the importation of goods produced by forced labour, including child labour.

Mexico “Resolution on the Elimination of Forced Labor in Global Supply Chains” (early 2023) – This resolution addresses the enforcement measures and compliance requirements to prevent the importation of goods produced through forced labour.

The European Union has postponed the implementation of its Deforestation Regulation by a year, moving the start date from December 2024 to December 2025. This regulation aims to prohibit the sale within the EU of products linked to deforestation, such as soy, beef, coffee, and palm oil. The delay grants companies additional time to ensure their supply chains are free from deforestation-related activities. Large operators and traders are now required to comply with the regulation by December 30, 2025, while micro and small enterprises have until June 30, 2026. This decision follows concerns from various stakeholders, including EU member states and trade partners like Brazil and Indonesia, about the feasibility of meeting the original deadline. While some industry groups view the postponement as necessary for adequate preparation, environmental organisations have criticised the delay, warning it could lead to continued deforestation in the interim. The European Commission has committed to exploring ways to reduce administrative burdens for companies and plans to implement an online system to facilitate compliance by December 2025.

On November 19, 2024, the Council adopted a regulation banning products made with forced labour. The regulation establishes a framework for inspecting human rights violations across supply chains. It also provides a legal mechanism to suspend the import and export of target goods made with forced labour at the EU’s borders and compel companies to withdraw goods already in the EU market.

CSDDD will start applying in 2027 to companies with over 5,000 employees and 1,500 million in turnover.

Germany plans to reduce the scope of its national supply chain due diligence legislation (LkSG), decreasing the number of firms impacted by the LkSG from 5,200 to fewer than 1,000. Replacing the LkSG with the CSDDD could violate EU law as legal experts note provisions of the CSDDD that prohibit lowering existing protections.

International Taxonomies: Key Developments in 2024

ASEAN:

The ASEAN Taxonomy Version 2 took effect in February 2024.

Australia:

ASFI’s sustainable finance taxonomy launched a second round of public consultation, seeking feedback on the draft climate change mitigation criteria for six priority sectors, along with generic criteria for “do no significant harm” and minimum social safeguards. The consultation closed on December 1, 2024. The initial Australian taxonomy for climate mitigation is scheduled for release by mid-2025, as outlined in the Government’s sustainable finance roadmap.

Brazil:

The Ministry of Finance has initiated the first public consultation on the Brazilian Sustainable Taxonomy (TSB) until January 31, 2025. The first stage of the public consultation focuses on selecting sustainable economic activities, integrating environmental, social, and equity criteria tailored to Brazil’s diversity. It includes reviewing the Monitoring, Reporting and Verification system for tracking sustainable capital flows and the Minimum Safeguard proposal for cross-cutting guidelines.

Canada:

The Government of Canada has announced plans to develop a made-in-Canada sustainable finance taxonomy aimed at mobilising private investment to support the country’s net-zero goals. Initially, the Taxonomy will concentrate on six hard-to-abate sectors: electricity, transportation, buildings, agriculture, manufacturing, and extractives, including natural gas, with a focus on significantly decarbonising existing operations. Canada’s Taxonomy is scheduled for development within 12 months and will be interoperable with global taxonomies.

Costa Rica:

The country launched a new Taxonomy focusing on climate change mitigation and adaptation activities across eight priority sectors including electricity, gas, steam and air conditioning supply, construction, transportation, manufacturing, solid waste and emissions capture, water supply and treatment, Information and communication technology (ICT) and land use (agriculture, livestock and forestry).

Hong Kong:

The Hong Kong Monetary Authority (HKMA) launched a new Taxonomy covering 12 economic activities and 4 sectors – power generation, transportation, construction, and water and waste management. It includes supplemental guidance with thresholds and criteria to be considered eligible under the Taxonomy. The Taxonomy is compatible with the Common Ground Taxonomy, EU Taxonomy, ASEAN Taxonomy, and Climate Bonds Taxonomy.

India:

The Reserve Bank of India (RBI) announced an upcoming climate finance taxonomy.

Israel:

The Ministry of Environmental Protection published a supplementary document for the taxonomy for a public review in March 2024. The document acts as a User Guide for the Israeli Taxonomy for Sustainable Activities.

Thailand:

The Thailand Taxonomy Board launched Phase 2 of the Thailand Taxonomy for public consultation, which aims to extend its scope to four key sectors: manufacturing, agriculture, waste management, and construction.

UK Green Taxonomy:

The HM Treasury launched a consultation in November 2024 on the UK Green Taxonomy. The primary purpose of the consultation is to establish how a national Taxonomy would be complementary to existing policies in meeting the objectives of mitigating greenwashing and channelling capital in support of the government’s sustainability objectives. The consultation will be open for 12 weeks from November 14, 2024 until February 6, 2025.

What’s in a Fund name?

SFDR gets a facelift

The EU Platform on Sustainable Finance published a briefing on December 17, 2024, proposing a new framework for categorising financial products under SFDR to address greenwashing concerns, with mandatory minimum criteria for each sustainability strategy. The new categories include “Sustainable,” “Transition,” “ESG Collection,” and “Unclassified Products,” each with specific criteria and indicators for measurement. Sustainable products must align with the EU Taxonomy or contribute to sustainable investments, passing DNSH tests and meeting exclusions based on EU Paris-Aligned Benchmarks (PABs). Transition products focus on assets aligned with credible net-zero pathways, including Taxonomy-aligned CapEx and science-based targets. ESG Collection products emphasise material sustainability features with engagement strategies for investments lacking transition plans.

The proposal introduces binding elements for each category, requiring Financial Market Participants (FMPs) to define relevant criteria, indicators, and thresholds to ensure compliance. Measurement indicators are closely tied to the EU Taxonomy, European Sustainability Reporting Standards (ESRS), and Climate Benchmarks, but specific minimum thresholds are still under review.

Social objectives remain less defined within the EU’s Sustainable Finance Framework, and further efforts are needed to integrate these into the categorization process. This includes analysing Principal Adverse Impacts (PAIs) and ESRS to identify actionable social indicators and thresholds.

The next steps involve refining thresholds for all SFDR products, focusing on diverse asset classes like insurance, pensions, and private market funds. Enhanced disclosures and reporting will include metrics such as Taxonomy alignment, PAI performance, exclusions, and engagement outcomes, ensuring transparency and accountability in sustainability reporting.

SEC’s top greenwashing cases

In 2024, the SEC took decisive steps to crack down on greenwashing, taking action against several firms misleading investors about ESG investment practices:

Invesco Advisers, Inc.:

The Atlanta-based investment adviser agreed to pay a $17.5 million civil penalty to settle charges of making misleading statements about the percentage of assets under management that integrated ESG factors in investment decisions.

WisdomTree Asset Management:

The New York-based firm was fined $4 million for misrepresenting the ESG strategies of three exchange-traded funds (ETFs). The SEC found that from March 2020 to November 2022, WisdomTree falsely claimed these funds did not invest in fossil fuel and tobacco companies, despite such investments being present.

Inspire Investing Inc.:

This Idaho-based investment fund, promoting “biblically responsible investing,” was fined $300,000 by the SEC for not adhering to its stated investment criteria. The SEC charged that Inspire did not perform adequate research to ensure investments complied with its principles, leading to inconsistent decision-making.

How to ESMA-fy sustainability funds

The ESMA Guidelines, effective November 2024, establish a formal system for qualifying funds using ESG or sustainability-related terms in their names, with oversight and enforcement by national regulators under a comply-or-explain basis. These guidelines apply to retail and institutional funds, including UCITS, Alternative Investment Funds, and index-tracking funds, and focus on sustainability strategies derived from the EU Climate Benchmarks. This includes normative screening for activities such as tobacco production, controversial weapons, and violations of UNGC/OECD principles (CTB exclusions) as well as strict thresholds for involvement in fossil fuel-related sectors like coal, oil, and gas (PAB exclusions).

Funds with ESG, sustainability, or impact-related terms in their names must allocate at least 80% of their investments to assets aligned with the fund’s sustainability strategy. Transition-related and impact-focused funds must also demonstrate measurable paths to social or environmental transition or generate positive, measurable impacts alongside financial returns.

These requirements aim to protect investors from greenwashing while promoting clarity and consistency in fund naming.

It should be noted that the ESMA Guidelines are exactly as stated - official “guidelines” - and may require interpreting strict revenue thresholds for fossil fuel-related activities, factoring in the detailed breakdown of sector-specific revenue data, data availability, and methods for assessing controversies or UNGC compliance risks.

Green Banking Developments in 2024

In 2024, several regions implemented key climate-related financial regulations, shaping the global ESG landscape. The EU Taxonomy alignment requirements for banks kicked off in January 2024, with ECB climate stress tests highlighting manageable transition risks but concerns about physical risks. In the US, the SEC mandated climate-related disclosures, focusing on material risks and emissions. The UK’s Transition Plan Taskforce released net-zero transition guidelines in October 2024, while Canada introduced sustainable investment guidelines and mandatory climate disclosures. Australia launched a sustainable finance taxonomy and conducted a climate risk survey in November. China expanded its carbon market to include more high-emission sectors, and India’s RBI proposed a draft framework for climate-related risk disclosures in February.

Global

Update of the Basel Core Principles for Effective Banking Supervision

In April 2024, the Basel Committee on Banking Supervision updated its Core Principles for Effective Banking Supervision to explicitly incorporate climate-related financial risks. The updated principles emphasise that banks should understand how climate-related risk drivers may manifest through financial risks, recognise that these risks could materialise over varying time horizons (potentially extending beyond traditional capital planning horizons), and implement appropriate measures to mitigate these risks. Supervisors are also expected to consider climate-related financial risks in their oversight, assess banks’ risk management processes, and require banks to submit information that facilitates the evaluation of the materiality of such risks.

European Union (EU)

ECB “Fit-for-55” Climate Stress Tests (November 2024)

The European Central Bank (ECB) concluded its “Fit-for-55” climate stress test, revealing that transition risks alone are unlikely to undermine the financial stability of the EU banking system. The test assessed the resilience of banks under various climate scenarios, showing that the risks associated with the EU’s climate policy targets (such as reducing emissions by 55% by 2030) could be managed effectively. However, physical risks like extreme weather events still pose a potential threat to financial stability.

United States (US)

Securities and Exchange Commission (May 2024)

The SEC adopted new climate-related risk disclosure rules on March 6, 2024, requiring public companies to disclose material climate-related risks, their mitigation efforts, and emissions data (Scope 1 and 2). The rules also mandate disclosure of severe weather-related financial impacts and require board oversight of climate risks. Unlike earlier proposals, Scope 3 emissions reporting is not required, though many companies may still disclose them voluntarily. These rules aim to improve the consistency and comparability of climate-related disclosures for investors.

United Kingdom (UK)

Transition Plan Taskforce Final Report (TPT) (October 2024)

The UK Transition Plan Taskforce (TPT) concluded its work in October 2024, releasing a final report with guidance on best practices for creating robust, science-based transition plans towards net zero. The report includes criteria for assessing the credibility of such plans, focusing on governance, risk management, and decarbonisation strategies. It provides valuable resources for companies looking to align their strategies with the UK’s climate goals. The TPT’s recommendations aim to standardise transition planning and enhance transparency.

Canada

Canadian Sustainable Investment Guidelines (October 2024)

On October 26, 2024, the Canadian government introduced sustainable investment guidelines and mandatory climate disclosures to support the transition to net-zero emissions by 2050. The guidelines aim to guide investments in clean and transition sectors, while large companies will need to disclose climate-related risks starting in 2025. These measures are part of a broader plan to boost sustainable economic growth and accelerate climate action.

Australia

Sustainable Finance Taxonomy (June 2024)

The Australian Government, in partnership with the Australian Sustainable Finance Institute (ASFI), is developing a sustainable finance taxonomy to guide investments in green and transition activities. The initial report, published in June 2024, outlines the governance, methodological framework, and stakeholder consultations. It covers technical screening criteria for key sectors like electricity, mining, and construction, aligned with climate goals. Key methodologies include defining green activities and incorporating social considerations. The project aims to establish clear guidelines for sustainable finance in Australia.

Australian Prudential Regulation Authority (APRA) (November 2024)

APRA’s 2024 Climate Risk Self-Assessment Survey, conducted with 149 responses from regulated entities, assessed how well Australian banks, insurers, and superannuation trustees are managing climate risks. Key findings show improvements in climate risk maturity, especially in governance and strategy. However, climate risk disclosure has seen a slight decline. The survey underscores the need for continued progress, with APRA planning to consult on updating prudential standards by 2025 to further integrate climate risk into risk management frameworks.

China

Carbon Market Expansion (September 2024)

In September 2024, China expanded its carbon market to include high-emission sectors like cement, steel, and aluminium, increasing coverage to 60% of national emissions. New regulations also introduced technical standards for emission reporting in cement industries. In parallel, China refined its voluntary emissions reduction mechanisms by coordinating renewable energy certificates and carbon trading systems. These changes aim to enhance market transparency and efficiency, helping China meet its carbon neutrality targets. The new sectors will start participating in 2024, while further regulatory updates are expected.

India

Reserve Bank of India (RBI) Draft Disclosure Framework on Climate-Related Financial Risks (February 2024)

In February 2024, the Reserve Bank of India introduced the draft ‘Disclosure Framework on Climate-Related Financial Risks’ to mandate disclosures by regulated entities. The framework focuses on governance, strategy, risk management, and targets for climate risk. It aims to integrate climate-related concerns into financial operations, helping entities align with sustainable practices. This framework is a key step in India’s ongoing efforts to enhance climate finance and promote climate risk management in the financial sector.

Nature & Biodiversity– the next frontier of sustainability reporting?

2024 – a Triple COP year

In 2024, the United Nations convened three pivotal Conferences of the Parties (COPs) to address the intertwined challenges of climate change, biodiversity loss, and land degradation.

Convention on Biological Diversity (CBD COP16) in Cali, Colombia

Delegates reached a historic agreement to involve Indigenous peoples in decisions related to nature conservation, establishing a new subsidiary body to facilitate inclusive decision-making. Additionally, a global fund was established to which companies using genetic data are expected to contribute, with half of the revenue allocated to Indigenous communities. However, the conference concluded without resolving key issues such as financial resource mobilisation and a global framework for progress monitoring, illustrating deep North-South divides.

UN Framework Convention on Climate Change (UNFCCC COP29) in Baku, Azerbaijan

Developed nations agreed to channel at least $300 billion annually into developing countries by 2035 to support their climate change mitigation and adaptation efforts. A significant achievement was the ratification of a framework under Article 6 of the Paris Agreement for trading UN-backed carbon credits between countries, potentially unlocking substantial climate finance. However, the summit faced criticism for the perceived inadequacy of financial commitments and the lack of concrete steps towards phasing out fossil fuels.

UN Convention to Combat Desertification (UNCCD COP16) in Riyadh, Saudi Arabia

A key outcome was the commitment of $70 million to advance the Vision for Adapted Crops and Soils (VACS), aiming to prevent topsoil loss and promote effective land restoration. Despite discussions, the conference concluded without an agreement on a global plan to address droughts, with deliberations postponed to the 2026 talks in Mongolia. These conferences underscored the urgency of coordinated global action to address environmental challenges, achieving notable progress while also highlighting persistent divisions and the need for continued dialogue.

TNFD Update: Growing Adoption and Sector-Specific Guidance

In 2024, the Taskforce on Nature-related Financial Disclosures (TNFD) achieved a significant milestone, with over 500 organisations globally - representing $17 trillion in assets under management (AUM) - adopting the TNFD framework to enhance nature risk reporting. This surge in adoption reflects a growing commitment by businesses and financial institutions to integrate biodiversity and ecosystem considerations into their decision-making processes. TNFD has also expanded its sector-specific guidance to aid diverse industries, including agriculture, mining, and construction, in assessing and disclosing nature-related risks.

The 2024 EY Nature Risk Barometer evaluates corporate disclosures against TNFD recommendations, revealing that while 94% of companies disclose nature-related information, full alignment remains low. Latin American firms lead globally in disclosure rates, followed by Canada and the U.S. The extractive and food sectors are top performers. The findings underscore the growing recognition of nature-related risks but highlight the need for deeper integration of TNFD standards into corporate reporting.

These developments reflect a broader trend in corporate governance, where companies are increasingly recognising the financial implications of environmental degradation. They also illustrate a shift towards “nature-positive” goals, aiming to restore ecosystems and maintain biodiversity while aligning business strategies with sustainability imperatives. This momentum is part of a larger movement to embed natural capital considerations into the global financial architecture, positioning nature as a critical asset to be safeguarded for long-term economic resilience.

Global ESG Ratings Regulations

ESG Ratings Regulation

The EU and India are the only jurisdictions regulating ESG ratings providers on a mandatory basis. While the EU regulation emphasises transparency in methodologies and conflict of interest prevention, India’s rules are more far-reaching, requiring ESG ratings products to align with the BRSR Core framework and mandating compliance with registration and ongoing adherence to the framework. This has led to multiple industry providers like Morningstar Sustainalytics and S&P quitting the ratings market in India due to the regulatory pressures. Meanwhile, across the Asia-Pacific, regulators are shaping voluntary regimes based on the IOSCO recommendations and ICMA principles. These frameworks provide ESG ratings providers with the flexibility to develop their own ratings methodologies, while ensuring they adhere to key principles related to internal controls, governance systems, and transparency.

Implications for smaller providers

The evolving regulatory landscape presents significant challenges for smaller ESG ratings providers. High supervisory fees remain a key barrier to entry, particularly for providers operating on limited resources. Exemptions from these fees are critical to ensuring broader market participation, but questions persist about their adequacy and scope. Additionally, establishing jurisdictional equivalence is essential to reduce the costs of compliance for smaller players operating across multiple regions. To support smaller providers, regulators must ensure that lighter-touch rules are applied and that regulatory frameworks are not overly complex or burdensome. Striking a balance between maintaining robust oversight and avoiding unnecessarily stringent requirements is vital to fostering innovation and competition in the ESG ratings market.

Conclusion

In 2024, ESG regulatory developments underscored a transformative shift in how organisations worldwide approach sustainability reporting. One of the most significant changes was the move from voluntary to mandatory reporting, spearheaded by the establishment of a global baseline for ESG disclosures by the International Sustainability Standards Board (ISSB) and the European Union’s Corporate Sustainability Reporting Directive (CSRD). These frameworks aim to standardise sustainability reporting across jurisdictions, providing clearer, comparable metrics for stakeholders. However, this shift has also introduced challenges, particularly for smaller companies that may lack the resources or expertise to meet stringent reporting requirements. As organisations struggle with the growing compliance burden, there is a heightened need for tailored tools and support to ensure that they can participate effectively in the evolving regulatory environment.

Efforts to address interoperability between different standards and frameworks also emerged as a critical focus in 2024. Aligning frameworks such as the ISSB’s standards, the CSRD, and sector-specific guidance like the TNFD is essential to reducing complexity and duplication in ESG reporting. These developments highlight the necessity of integrated solutions that allow companies to meet diverse stakeholder needs. Interoperability also paves the way for a more efficient and transparent global reporting ecosystem, facilitating consistent data flows and actionable insights across markets.

For platforms such as ESG Book, the developments of 2024 reinforce the critical need for scalable, user-friendly reporting tools that can assist companies, banks, and investors in managing the growing ESG reporting burden. As ESG disclosures become increasingly complex and mandatory, ESG Book offers a streamlined solution that enables businesses to efficiently navigate reporting and compliance challenges. By automating and simplifying the data collection and reporting process, ESG Book alleviates the pressure on companies that lack the resources and expertise to meet ever more stringent ESG requirements.

For companies

ESG Book’s platform enables seamless integration with various regulatory frameworks, such as the ESRS, ISSB, SASB, GRI, TCFD, and EU Taxonomy, ensuring that sustainability reports are in full compliance with the latest standards. The platform provides clear, actionable insights to help companies meet their reporting obligations, while reducing the risk of errors or omissions. It allows businesses to focus on their sustainability efforts, knowing their reporting is accurate and aligned with global best practices.

For banks and investors

ESG Book delivers powerful analytics tools that can assess the ESG performance of portfolios and identify potential risks and opportunities. With ESG Book’s platform, financial institutions can gain a clear view of the ESG credentials of companies they invest in, ensuring informed decision-making. By consolidating data from diverse sources and frameworks, ESG Book makes it easier to track the evolving regulatory landscape and assess the performance of companies against investor expectations and regulatory requirements.

Looking ahead, the 2025 deadlines for mandatory compliance under the CSRD and ISSB frameworks mark a critical juncture for organisations. Companies face significant pressure to enhance their data collection, reporting, and governance processes to align with these new standards. The year ahead will demand heightened collaboration between regulators, businesses, and technology providers to support organisations—especially smaller ones—in achieving compliance.

ESG Book plays a pivotal role in supporting the entire ESG ecosystem. By offering a single, seamless platform that bridges the gap between complex standards and real-world applications, ESG Book helps companies, banks, and investors mitigate the growing reporting burden, enabling more transparent, accountable, and sustainable practices across markets. As the regulatory landscape evolves, this is increasingly vital in fostering trust among stakeholders and driving long-term, sustainable growth.

Read More Research

Beyond 1.5˚C*