The New Global Baseline?

“Updates to sustainability standards in 2022 brought with them increased sectoral specificity, simplifying the process for firms trying to understand which topics and metrics are most material to their operations.”

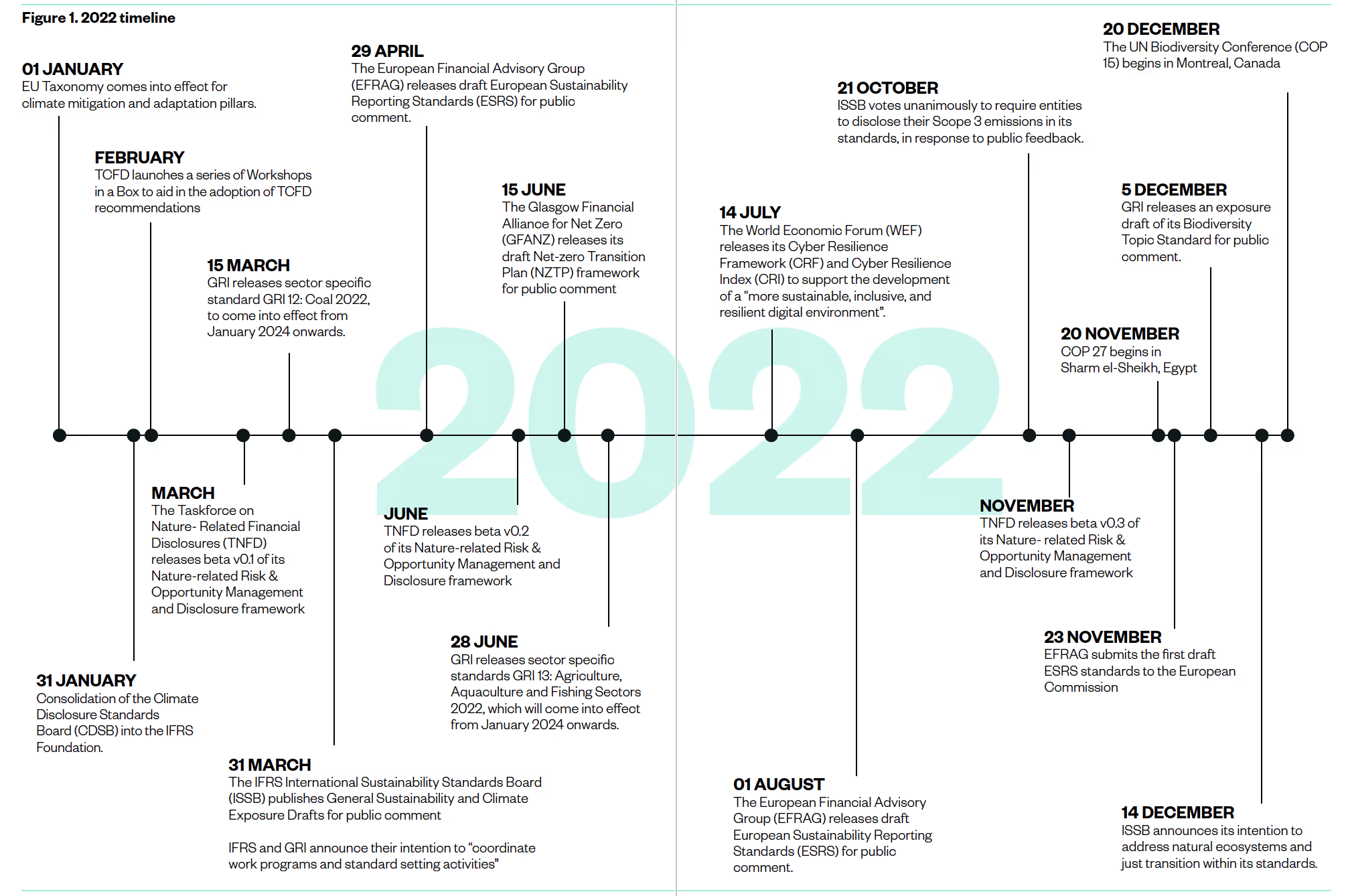

With updates announced for several major ESG frameworks and standards, in an effort to streamline and simplify the corporate disclosure process, 2022 marked a year of development across the corporate sustainability reporting landscape.

This article provides an overview of key developments in ESG frameworks and standards over the past year and discusses some of the trends that will shape the terrain in the years to come.

Consolidation, Collaboration, and Convergence

The plethora of reporting frameworks and standards for disclosure can be difficult for corporates and investors to navigate.

Standard-setters are taking notice and are working to ease the reporting burden by streamlining disclosure recommendations. One such example of industry convergence in 2022 was the release of the IFRS International Sustainability Standards Board (ISSB) General Sustainability (S1) and Climate (S2) Exposure Drafts for public consultation in March1.

Rather than “reinventing the wheel”, the proposed standards are aligned with widely used frameworks and standards to facilitate easy adoption. Specifically, the Climate Exposure draft is closely aligned with the Taskforce for Climate-related Financial Disclosures (TCFD) framework, with sector specific metrics drawn from the Sustainability Accounting Standards Board (SASB)2. With regulators around the world increasingly advocating for TCFD-aligned climate disclosure, the inclusion of TCFD recommendations within the ISSB proposed standards has the potential to align with jurisdictional requirements, thereby streamlining the disclosure process for entities.

On a similar note, the European Financial Reporting Advisory Group (EFRAG) released its draft European Sustainability Reporting Standards (ESRS) for public feedback in April 20223. The ESRS standards will be mandatory for applicable companies within the European Union (EU). In order to simplify the adoption of the ESRS for firms that report in accordance with the Global Reporting Initiative (GRI), the GRI and EFRAG have been working closely together to ensure the interoperability of reporting standards4.

Prioritization of biodiversity-related disclosure

2022 also brought an increased focus on biodiversity and the preservation of natural ecosystems. The UN Biodiversity Conference (COP15) was held in Montreal, Canada from December 7-19, resulting in the Kunming-Montreal Global Biodiversity Framework.5 Realizing the business risk posed by biodiversity loss, framework providers and standard-setters have been looking to introduce biodiversity-related reporting recommendations. For example, the Task Force on Nature-related Financial Disclosures (TNFD) released beta iterations of its Nature-related Risk & Opportunity Management and Disclosure Framework6 for public consultation. Similarly, to support robust biodiversity disclosure practices, the GRI is working on updating its Biodiversity Topic Standard to reflect

“internationally agreed best practices [that] align with recent developments as well as relevant authoritative intergovernmental instruments in biodiversity.”9 The draft Biodiversity Topic Standards have been released for public comment from December 5 2022 - February 28 2023. In keeping with the momentum around biodiversity-related disclosure, the ISSB appointed two Special Advisers, Karin Kemper and Geordie Hungerford to guide their work on natural ecosystems and just transition, as the organization commits to researching enhancements to support the S2 Climate standard in this area.10

Release of Sector-specific Reporting Standards

Updates to sustainability standards in 2022 brought with them increased sectoral specificity, simplifying the process for firms trying to understand which topics and metrics are most material to their operations. This is evident within the latest iteration of the GRI standards. The 2021 update to the GRI Universal Standards was followed by the Sector Standard for Oil and Gas,7 the first of forty planned sector standards. Two new Sector Standards (Coal,

and Agriculture, Aquaculture, and Fishing) were released in 2022. The GRI Sector Standards aim to add clarity on “likely material topics” for firms, based on their sectors, and can support organizations in their materiality assessments.8

Similarly, the incorporation of the SASB standards into the ISSB S2 Climate Exposure Draft forms the basis of a set of industry-specific metrics, designed to address relevant ESG topics for 77 industries, utilizing a financial materiality approach. Furthermore, in an effort to define material SDG-related topics for different economic sectors, the Global Investors for Sustainable Development Alliance (GISD) conducted a study to define a set of ESG reporting indicators to assess progress towards the SDGs by companies in specific sectors.11 These metrics were added to ESG Book in July,12 and are currently available for companies to disclose against.

Additionally, 2022 marked the year EU Taxonomy Climate Mitigation and Climate Adaptation disclosure requirements were applicable for entities across thirteen economic sectors, with companies beginning to publish reports in 2023 for the 2022 financial year.13

Figure 1. 2022 timeline

2023 Outlook: Stay Tuned for Upcoming Developments in Sustainability Reporting Frameworks and Standards

2023 brings with it more changes on the horizon, as frameworks and standards come into effect, and new updates are released.

Specifically, corporates can look forward to reporting in line with the GRI 2021 Universal Standards from January 1 2023, onwards.14 The GRI revised Universal Standards are now available for disclosure on ESG Book. Similarly, the EU Corporate Reporting Sustainability Directive (CSRD) entered into force on January 5 this year. Corporate entities will start to apply CSRD for reports published in 2025, for 2024 disclosures.15

Additionally, both ISSB and ESRS standards are likely to be finalized in June this year. The European Commission announced that it would adopt the final ESRS standards as delegated acts.16 Similarly, IFRS chair Erkki Liikanen stated the intention for the ISSB to have the final S1 and S2 standards ready by June, at the World Economic Forum in Davos this January.17 ISSB standards will go into effect from January 2024 onwards.18 Looking ahead in the year, the GRI Mining Standard is likely to be finalized in Q4.19

Figure 2. 2023 Standard-setting milestones

In an ever-evolving sustainability reporting landscape, 2022 brought clarity to reporting recommendations, streamlining standards, and simplifying the disclosure process. New frameworks and standards were launched like the GRI sector-specific standards, and the TNFD beta framework releases, while existing recommendations were updated and enhanced. These changes will carry into 2023 and beyond, as we see a convergence in ESG metrics with the finalization of the ISSB and CSRD standards. This is going to be a significant step towards developing a global baseline for sustainability standards, streamlining the corporate reporting process, and de-mystifying the alphabet soup of reporting frameworks and KPIs.